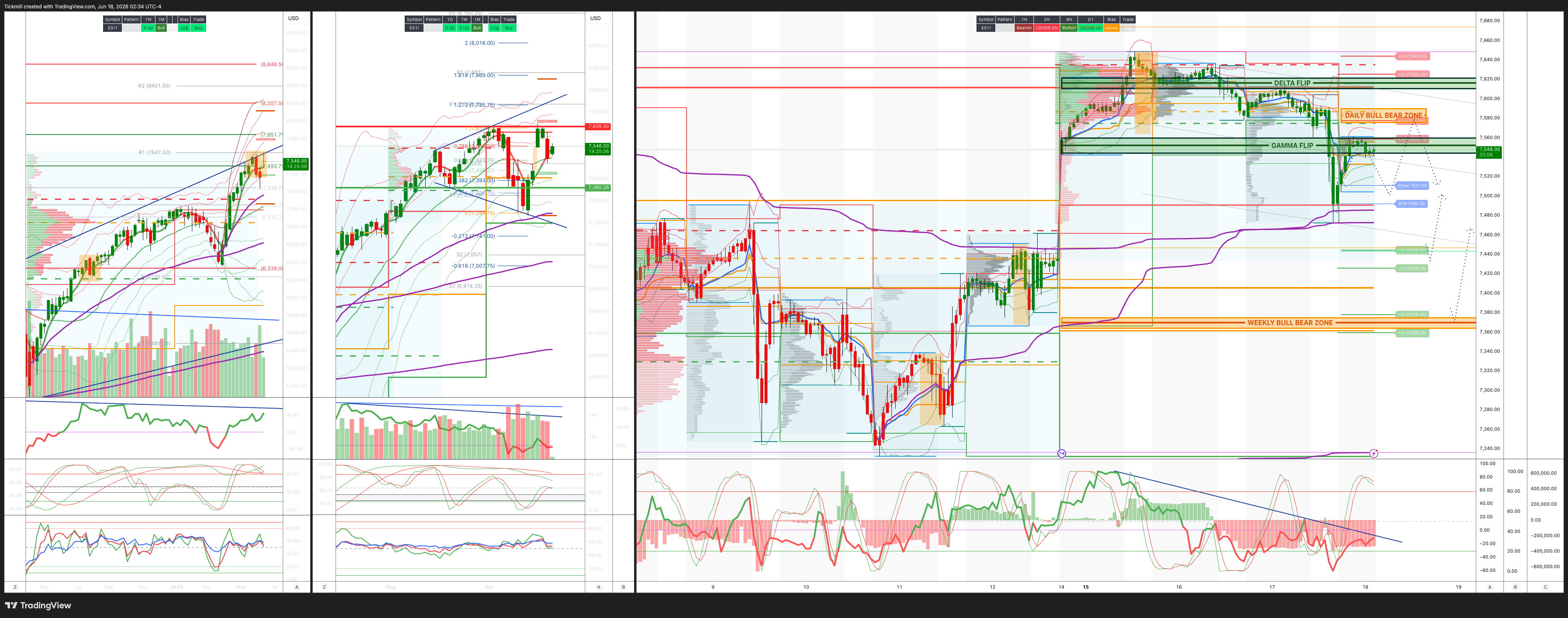

S&P500 Daily Action Areas & Price Targets 18/6/26

S&P500 Daily Action Areas & Price Targets 18/6/26

***QUOTING ES1! FOR CASH US500 EQUIVALENT LEVELS, SUBTRACT POINT DIFFERENCE***

WEEKLY BULL BEAR ZONE 7365/75

WEEKLY RANGE RES 7635 SUP 7360

June MOPEX Straddle: 274pt range implies a OPEX to OPEX range of [7134, 7683]

June QOPEX Straddle is 546.4pt giving us a range of [5960,7052]

JHEQX Q2 Collar 6189/6290 - 6865/6955

DEC2025 OPEX to DEC2026 OPEX is 945 points giving us a range of [5889,7779]

SPX PUT/CALL RATIO 1.28 (The numbers reflect options traded during the current session. A put-call ratio below 0.7 is generally considered bullish, and a put-call ratio above 1.0 is generally considered bearish)

DAILY VWAP BEARISH 7530

WEEKLY VWAP BEARISH 7474

MONTHLY VWAP BULLISH 7036

DAILY STRUCTURE - OTFL - 7604

WEEKLY STRUCTURE - OTFH

MONTHLY STRUCTURE - OTFH - 7199

Balance: This refers to a market condition where prices move within a defined range, reflecting uncertainty as participants await further market-generated information. Our approach to balance includes favouring fade trades at the range extremes (highs/lows) while preparing for potential breakout scenarios if the balance shifts.

One-Time Framing Higher (OTFH): This represents a market trend where each successive bar forms a higher low, signalling a strong and consistent upward movement.

One-Time Framing Lower (OTFL): This describes a market trend where each successive bar forms a lower high, indicating a pronounced and steady downward movement.

DAILY BULL BEAR ZONE 7580/90

GAMMA FLIP 7550

DELTA FLIP 7614

DAILY RANGE RES 7579 SUP 7443

2 SIGMA RES 7647 SUP 7375

VIX BULL BEAR ZONE 19

TRADES & TARGETS

SHORT ON REJECT/RECLAIM DAILY BULL BEAR ZONE TARGET RTH CLOSE

LONG ON REJECT/RECLAIM DAILY RANGE SUP TARGET RTH CLOSE

***ADDITIONAL SETUPS & TARGETS HIGHLIGHTED ON THE CHARTS***

(I FADE TESTS OF 2 SIGMA LEVELS ESPECIALLY INTO THE FINAL HOUR OF THE NY CASH SESSION AS 90% OF THE TIME WHEN TESTED THE MARKET WILL CLOSE ABOVE OR BELOW THESE LEVELS)

GOLDMAN SACHS TRADING DESK VIEW - ‘Eventful Start’

Warsh’s first FOMC was an eventful and meaningfully hawkish debut. Rates were left unchanged, as expected, but the communication regime changed quickly. The statement was shorter, the emphasis shifted firmly toward “price stability,” and the market interpreted the press conference as a clear attempt to re-anchor inflation credibility. The result was a sharp repricing of the policy path, with markets now pricing almost two hikes by Q1 2027. Equities and EUR both sold off hard, with SPX down about 1.2% and EUR down roughly 0.9%, the worst FOMC-day reaction for both compared with prior meetings this year.

The most important takeaway is that the rate decision was not the event; Warsh’s reaction function was the event. The market already expected a hold, but it did not fully price a chair who would begin his tenure by emphasizing price stability so forcefully. That changes the near-term policy debate from “how soon can the Fed eventually cut?” to “how much tightening risk still needs to be embedded?” The fact that the curve now prices almost two hikes by Q1 2027 shows that investors took the message as materially more hawkish than the prior framework.

The dot plot was unusual and politically important. There were 18 votes, with 9 signaling a hike in 2026, while Warsh did not submit a dot. That non-submission is notable because it avoids mechanically anchoring the market to the new chair’s personal rate forecast, but it does not make the outcome dovish. If anything, it forces investors to infer Warsh’s stance from the statement and press conference, both of which leaned hawkish. The median may be less important than the distribution: half the dots pointing toward a 2026 hike tells the market that the Committee is no longer treating the current rate setting as obviously restrictive enough.

The announcement of new task forces on Fed communications, data, inflation and productivity, and AI is also important. This signals that Warsh is not just changing the tone of policy; he may be preparing to review the Fed’s analytical framework. The AI and productivity angle matters because it could affect estimates of potential growth, neutral rates, and inflation persistence. If the Fed concludes that AI is raising productivity meaningfully, it could tolerate stronger growth without seeing it as inflationary. But if the Fed instead focuses on AI capex, power demand, fiscal impulse, and financial conditions as inflationary forces, the policy floor could stay higher for longer.

The immediate market reaction followed the classic hawkish-Fed template. Front-end rates repriced higher, the dollar strengthened, EUR and JPY weakened, and equities sold off. The initial response to the statement was more contained, but the press conference drove the larger move as Warsh repeatedly emphasized price stability. That distinction matters because it suggests the market was not simply reacting to a few words in the statement; it was updating its view of the new chair’s policy instinct.

The severity of the SPX and EUR selloff versus prior FOMC meetings this year shows that this was a true regime test. Earlier meetings were mostly about timing and patience within an established framework. This meeting introduced uncertainty around the framework itself. The market now has to handicap not only the next rate move, but also how Warsh wants to reshape Fed communication, inflation analysis, and the balance between growth tolerance and inflation credibility.

For equities, the message is not outright bearish, but it is a clear tightening of the valuation backdrop. A market sitting near highs, with VIX recently crushed, poor top-of-book liquidity, and Tech still crowded, is vulnerable to a hawkish communication shock. Long-duration growth, AI, Semis, and high-beta momentum are the obvious areas of pressure if front-end hikes become more embedded. The recent rotation into Financials, Industrials, and rate-sensitive laggards may also become more complicated if the Fed is perceived as leaning against easing financial conditions.

The impact on Mega-Cap Tech is nuanced. On one hand, higher front-end pricing and a stronger dollar are headwinds for long-duration earnings and high-multiple AI exposures. On the other hand, the AI capex cycle remains a powerful earnings support, and lower oil still helps the inflation backdrop. The risk is that the market starts demanding more evidence of free-cash-flow conversion and return on invested capital from AI beneficiaries, rather than simply rewarding top-line growth and capex momentum. A hawkish Fed reduces the tolerance for expensive, crowded, and financing-sensitive stories.

FX is a key confirming signal. EUR and JPY weakness alongside a stronger dollar reflects a broader repricing of US policy divergence. The ECB and BOJ dynamics matter, but the dominant impulse was the Fed. If Warsh’s Fed is seen as more price-stability focused and less willing to validate cuts, the dollar can remain supported, particularly against currencies where domestic central banks are constrained or less hawkish. The fact that EUR’s selloff was worse than prior FOMC reactions this year underscores how underpriced the communication risk was.

FX volatility was also important because implied gap pricing was higher than usual into the event, reflecting uncertainty around the new chair. That proved justified. New-chair FOMCs are not just normal macro events; they are reaction-function discovery events. The market had to price the possibility that Warsh would alter the tone of the Fed, and he did. This should keep event-risk premia elevated around upcoming Fed communications, inflation data, and any speeches that clarify the role of the new task forces.

The rates takeaway is that the “higher floor” thesis gained credibility. Even without an immediate hike, the Fed has made it harder for the market to price a return to cuts. If nearly two hikes are now priced by Q1 2027, the front end is saying the balance of risks has shifted toward additional restriction. That is a meaningful change from a market that had been leaning on lower oil and geopolitical de-escalation as reasons for policy patience. Warsh effectively reminded investors that falling oil is helpful, but not enough to declare victory on inflation.

The task force on inflation and productivity could become the most important medium-term development. If the Fed is revisiting how to measure underlying inflation in an economy affected by AI, supply-chain rebuilding, energy shocks, and fiscal industrial policy, then traditional core metrics may become less decisive. Markets will need to understand whether Warsh’s Fed views AI primarily as disinflationary productivity improvement or as inflationary investment demand. That interpretation will have major implications for neutral rates, curve shape, and equity multiples.

The bottom line is that Warsh’s debut was a hawkish hold with framework-change risk. The Fed did not hike, but it shifted the market toward pricing almost two future hikes, emphasized price stability, delivered a shorter statement, and launched task forces that could reshape communication and inflation analysis. The immediate result was a stronger dollar, weaker equities, weaker EUR and JPY, and a sharper FOMC-day selloff than any prior meeting this year. The next phase depends on whether Warsh walks this back in subsequent communications or reinforces it. For now, the market has to treat the Fed put as further out of the money and the policy floor as meaningfully higher.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!